")

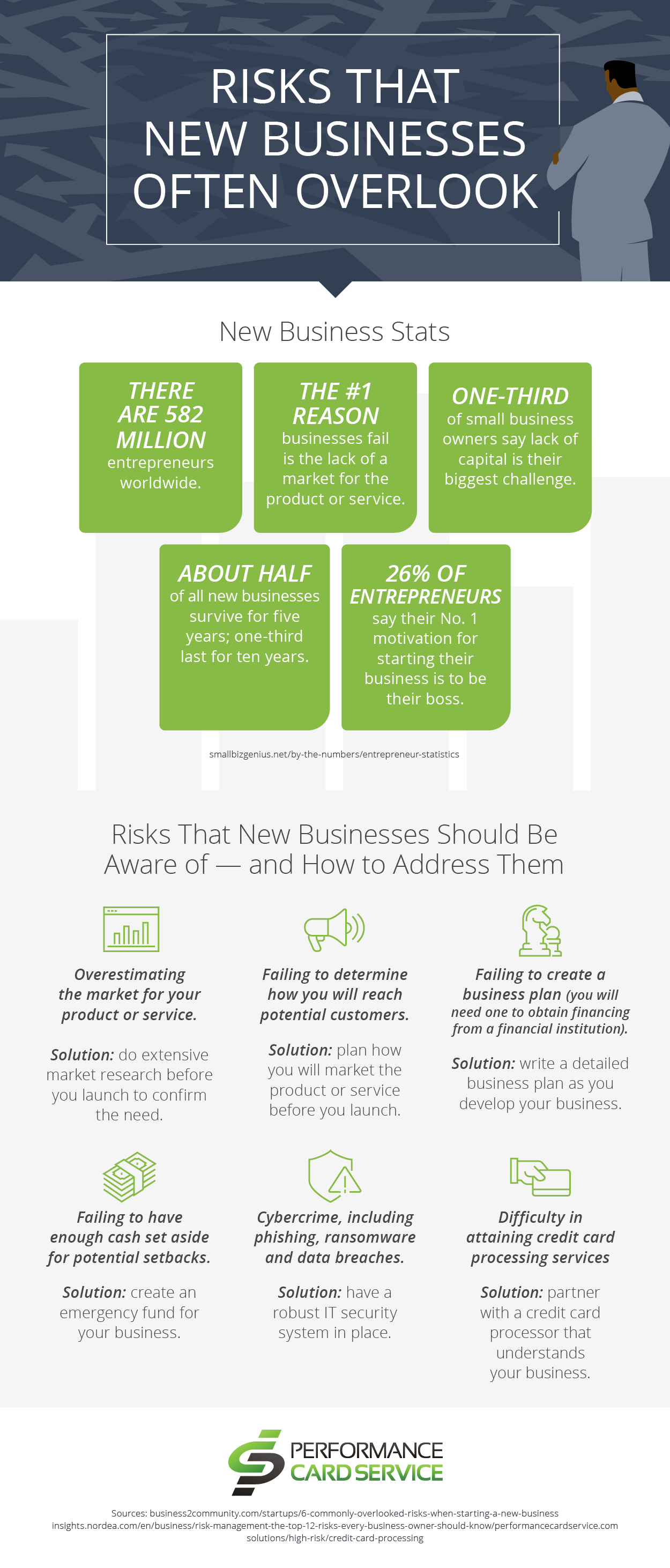

Thinking of starting a new business? You’re not alone — there are more than 580 million entrepreneurs worldwide. Maybe you’ve discovered an underserved niche in the market for one’s services, or perhaps you have a product that will make customers’ lives easier. Or maybe you simply want to be your boss — one in four business owners say that’s their biggest motivation for starting their business.

While the reasons to start a business vary, the fact is that many of them fail. In fact, nearly one in four will fail in the first year, and about half fail during in the first five. One of the common reasons is that there is no market need for the product or service, but there are other risks in which business owners are not aware. Here is a closer look at some of the overlooked risks to be mindful of when starting your business.

While every new business starts with a great idea, ideas are not enough to succeed.

You need a plan — ideally, a detailed business plan that includes information about your service or product, the market for it and a mission statement. It should also include a background about your employees, location and leadership team. Incorporate information about your plans for growth and financial position if you will seek financing. Having a marketing plan in place can help ensure that you get the product or service in front of customers who need it.

Another consideration? Your new business may have little or no credit history which can make it difficult to create a relationship with a financial institution to process credit cards. In this case, a high-risk credit card processing service can help with this aspect. The attached resource, Risks That New Businesses Often Overlook, describes more about this.

Graphic created by Performance Card Service.